A lot of people feel uneasy about tapping their phone to pay. You are not inserting a card, not entering a PIN, not doing anything that feels deliberate. You just hold your phone near a terminal for half a second and walk away. It seems too easy to be safe.

The reality is almost the opposite. Paying by phone is one of the most secure payment methods available, and in several measurable ways it is safer than swiping a card or even inserting a chip. Here is what is actually happening when you tap, and where the genuine risks come from.

What Actually Happens When You Tap

When you add a card to Apple Pay or Google Wallet, your real card number is never stored on your phone and never sent to the payment terminal. Instead, the wallet creates a token, a unique virtual stand-in for your card, that lives in a dedicated secure chip inside your device, isolated from everything else.

When you tap, your phone sends that token plus a one-time encrypted code generated specifically for that transaction. The terminal passes both to your bank, which verifies the code and approves the payment. The code is mathematically tied to that exact transaction and expires the moment it is used. Intercepting it is pointless because it cannot be reused.

The retailer never receives your card number. Nothing in the system transmits your actual card number. What sits in a retailer's records after you pay is a meaningless token.

This is fundamentally different from handing over a physical card, where your card number, name, and expiry date are visible to anyone who looks, or from swiping a magnetic stripe, which sends your real card details to the terminal in plain form.

Why It Is More Secure Than a Physical Card

The most common card fraud does not come from sophisticated technical attacks. It comes from skimming devices on card readers, stolen cards tapped at terminals, and data breaches at retailers who stored card numbers carelessly.

Phone payments are genuinely resistant to all of these. There is no card number to skim. There is no card number stored at the retailer to steal. If a retailer suffers a breach, your details are not in it.

There is also the matter of authentication. A physical contactless card requires no biometric check for purchases below a certain limit. Steal someone's wallet and you can tap their card immediately. Steal their phone and you cannot authorise a single payment without their Face ID, fingerprint, or PIN. That protection applies to every transaction, regardless of amount.

The Real Risks Worth Knowing

The risks that do exist are different from what most people worry about.

Malware on your device is the most credible threat. In 2025, researchers documented attacks where criminals tricked users into downloading fake banking apps. The malware used the phone's own NFC system to relay card information to the attacker, who then made payments remotely. This required the victim to download a malicious app and enter card details into it. The defence is simple: only install apps from the official App Store or Google Play, and never enter card details into any app you are not certain is legitimate.

Compromised account credentials are another real risk. If an attacker gets into your Apple ID or Google account, they could potentially add your card to a device they control. Strong passwords and two-factor authentication on those accounts close this off.

NFC eavesdropping, where someone nearby intercepts your payment signal, is the attack people most commonly fear and the one least worth worrying about. NFC works at a range of a few centimetres, requires you to actively initiate the transaction, and would only capture an encrypted one-time token that is already expired. Security researchers have demonstrated the concept in labs. Real-world fraud using this method is essentially undocumented.

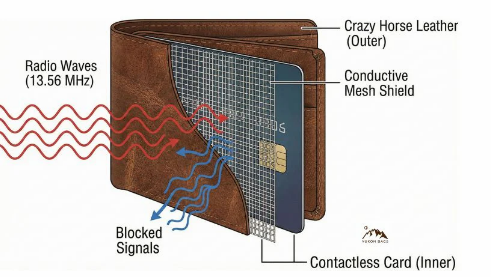

A Word on RFID-Blocking Wallets

They do nothing for phone payments. Phone payments are authorised by biometrics and use one-time tokens, so blocking the signal adds no protection. If you carry physical contactless cards and want peace of mind about those, an RFID wallet is a reasonable purchase. For your phone, it is irrelevant.

What Actually Matters

The security built into phone payments is robust, but it works best when a few habits are in place.

Keep your phone locked with Face ID, a fingerprint, or a strong PIN. This is the primary barrier between a thief and your cards. A phone with no lock screen is a serious exposure.

Keep your operating system updated. Security patches regularly address vulnerabilities that could affect payment systems.

Turn on transaction notifications from your bank. Real-time alerts let you spot anything unusual the moment it happens rather than weeks later when you check your statement.

Only add cards through official wallet apps directly from your bank or card issuer. Be sceptical of any third-party app asking to handle your card details.

So Is It Actually Safe?

Yes, genuinely. Major banks, payment networks, and independent security researchers all consider mobile wallet payments to be at least as secure as chip-and-PIN and significantly more secure than magnetic stripe or physical contactless cards. The token system protects your real card number at every step. The biometric requirement means a stolen phone stays useless for payments. The one-time codes mean intercepted data cannot be replayed.

The risks that exist are almost entirely about your device. Keep it locked, keep it updated, and be careful about what you install. Do those things and tapping your phone to pay is as safe as anything in your wallet and safer than most of it.

Frequently Asked Questions

Can someone steal my card details with a hidden NFC reader?

In practice, no. Your phone does not transmit payment data until you actively authorise the transaction with your biometric or PIN. Even if something were intercepted, it would be a one-time encrypted token that has already expired and cannot be reused.

What should I do if I lose my phone?

Remove your cards remotely immediately. In Apple Pay this is done through iCloud settings. In Google Wallet it is done through your Google account. Until then, your cards are safe because no one can make a payment without your biometrics or PIN, but removing them takes any remaining risk off the table.

Is phone payment safer than a physical card?

In several concrete ways, yes. Physical cards transmit your actual card number. Phone payments transmit a one-time token. Physical contactless cards can be tapped without any authentication for small purchases. Phone payments always require biometric or PIN approval. And retailers never hold your real card number after a phone payment transaction.

Can I use tap and pay if my phone battery is dead?

Generally no. Apple Pay has an Express Transit mode that works on very low battery for transport payments in supported cities, but standard retail payments require the phone to be powered on and unlocked. If you rely heavily on phone payments, keeping your battery topped up is worth the habit.

Do free banking apps from my bank store my card details?

The official app from your bank adds your card to Apple Pay or Google Wallet securely, with tokenisation handled by the wallet provider. Your actual card number is not stored by the app or on your device. This is distinct from unofficial third-party apps, which should be avoided for card management entirely.

Discussion (0)

Be the first to comment.