A virtual account gives businesses a simple way to track payments without opening multiple physical bank accounts. It works as a digital sub-account that routes every payment directly into one primary account.

This setup helps companies organize transactions, automate reconciliation, and manage cash more efficiently.

1) Overview of virtual accounts

A virtual account functions as a digital layer on top of a real bank account. It does not hold funds but directs every payment to the parent account while keeping the source identifiable.

How virtual accounts work

Each virtual account comes with a unique account number. When customers send payments, the bank routes the money to the primary account and tags it with the matching virtual account ID for easy tracking.

2) Why businesses use virtual accounts

Organizations use virtual accounts because they improve transparency and reduce manual work.

Faster reconciliation

Virtual accounts let businesses match incoming payments to the right customer quickly. Automated tagging helps reduce human error and speeds up bookkeeping.

Better cash management

Separating payments by customer or department gives companies clearer visibility into cash flow. This structure supports better financial planning and resource allocation.

Lower operational costs

Companies avoid paying fees for multiple physical accounts. Managing everything under one primary account cuts administrative overhead.

3) Types of virtual accounts

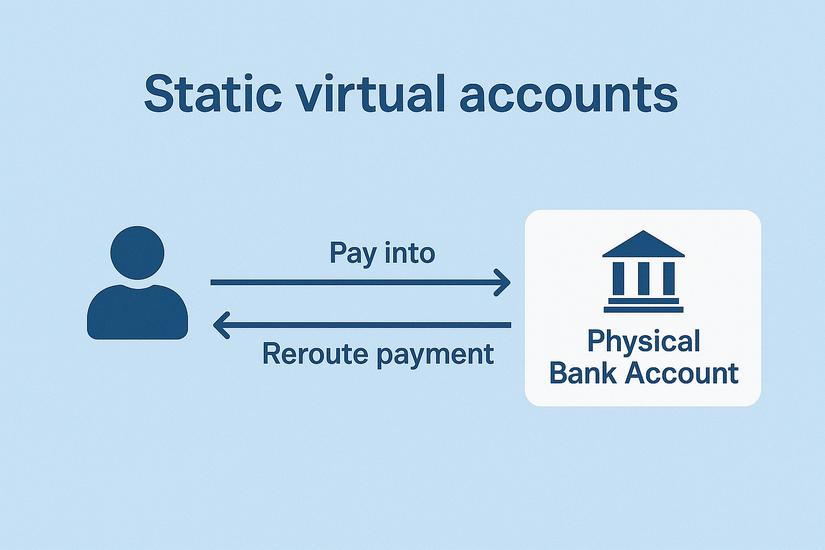

Static virtual accounts

A static virtual account keeps the same account number permanently. Subscription businesses and recurring-billing platforms often use these identifiers for predictable payments.

Dynamic virtual accounts

A dynamic virtual account generates a new number for each invoice or transaction. This setup works well for e-commerce, one-time payments, and high-volume merchants.

4) Virtual accounts vs traditional bank accounts

A traditional business account holds funds, earns interest, and supports full banking functions. A virtual account only acts as an identifier for routing payments into the primary account.

When to use each

Companies should use a standard business account for payroll, payouts, or regulatory needs. Virtual accounts work best when the goal is accurate tracking and fast reconciliation.

5) Common use cases for virtual accounts

E-commerce and online payments

Online retailers use virtual accounts to track customer orders and reduce disputes from misapplied payments. Clear identifiers make it easier to match each payment to the right order.

Subscription services

Membership and SaaS platforms assign virtual account numbers to subscribers to streamline recurring billing. This setup improves renewal tracking and reduces failed-payment confusion.

Marketplace platforms

Marketplaces use virtual accounts to separate seller payments, making settlements easier and faster. Each seller can receive payments under a unique virtual account reference.

Corporate treasury management

Large organizations use virtual accounts to structure internal cash pools and centralize funds while maintaining clear reporting. This supports better liquidity management and internal chargeback models.

6) How to set up a virtual account

Choose a bank or payment provider

Pick a provider that supports virtual account creation, multi-currency routing, and API integrations. Look for reporting tools that fit your accounting system.

Complete KYC and documentation

Banks require identity verification, business details, and compliance information before activating virtual accounts. Make sure you provide accurate and up-to-date documents.

Create virtual accounts for customers or transactions

Providers let you generate individual virtual account numbers for each customer or invoice. Clear labeling helps avoid confusion later.

Integrate with your finance systems

Connect virtual accounts to your ERP or accounting tools. Integration automates reconciliation and improves accuracy.

7) Risks and considerations

Compliance and regulatory differences

Rules vary by region, especially for cross-border payments. Businesses should confirm that their provider supports the regulatory requirements for their market.

Security and fraud prevention

Virtual accounts reduce exposure by avoiding multiple physical accounts. However, companies must protect access credentials and monitor suspicious activity.

Operational complexity

Without proper mapping, businesses may misroute payments or create duplicate identifiers. Strong internal processes prevent these issues.

8) Future of virtual accounts in banking

Embedded finance integration

Fintech platforms rely on virtual accounts for instant payments and seamless in-app financial services. This integration makes banking feel like a built-in feature instead of a separate step.

Real-time and cross-border expansion

More banks now support virtual accounts in multiple currencies, improving global payment speed and clarity. This helps businesses manage international customers more easily.

AI-driven automation

AI tools will automate reconciliation, detect anomalies, and deliver forecasts based on virtual account activity. This reduces manual work and improves decision-making.

FAQs

Can a virtual account hold money? No. All funds sit in the main account. The virtual account only serves as a routing identifier.

Are virtual accounts safe? Yes. They reduce exposure by consolidating funds into one protected account. Strong authentication and access controls add extra security.

Do individuals use virtual accounts? Most virtual accounts support business use cases, but individuals may encounter them when paying invoices or online merchants. The underlying routing still goes through a primary business account.

Summary

- Virtual accounts act as digital identifiers linked to a main account.

- They route payments cleanly for faster reconciliation.

- Businesses use them to organize customers, departments, and transactions.

- Static and dynamic versions support different payment models.

- Setup involves choosing a provider, completing verification, generating virtual accounts, and integrating systems.

Conclusion

Virtual accounts give businesses a simple way to track payments without increasing banking complexity. They improve reconciliation speed, cut costs, and support modern digital payment flows.

Most companies can start using virtual accounts quickly, and the setup process usually takes just a few steps. With strong accounting integration and clear internal processes, virtual accounts help teams maintain clearer cash management and more efficient operations.

Discussion (0)

Be the first to comment.